Correct Valuation in Insolvency and Liquidation: Why the IBBI's New Valuation Architecture Matters More Than It First Appears

Abstract

Valuation is one of the central mechanisms through which insolvency and liquidation processes allocate bargaining power, discipline decision-making, and shape recoveries. A recent series of interventions by the Insolvency and Bankruptcy Board of India — including the revised definition of fair value, the coordinating valuer mechanism, the notification of the International Valuation Standards, the Valuation Report Identification Number regime, and board-prescribed reporting discipline — amounts to a structural overhaul of India’s insolvency valuation ecosystem. This article argues that these reforms are among the most important procedural changes in the current insolvency reform cycle. They improve coherence, comparability, and verification in important ways, but they do not by themselves solve the harder problem of valuation reliability in practice. The article examines what the reforms change, why valuation correctness matters so deeply in CIRP and liquidation, and where the new framework still faces unresolved risks.

I. Introduction: Why Valuation Sits at the Centre of Insolvency Credibility

In insolvency and liquidation, valuation is never just a technical number. It is one of the key points at which the system decides whether it deserves to be trusted.

A weak valuation does not stay confined to a report. It distorts bidding behaviour, weakens creditor judgment, complicates judicial scrutiny, and increases the risk that the process will deliver outcomes that are formally compliant but commercially unconvincing. In the Corporate Insolvency Resolution Process, valuation shapes how the Committee of Creditors compares plans, assesses downside risk, and decides whether a resolution proposal is meaningfully preferable to liquidation. In liquidation, it influences reserve discipline, realisation strategy, and the credibility of recoveries themselves. Poor valuation can therefore infect the process long before anyone openly identifies it as the problem. [1]

That is why the Insolvency and Bankruptcy Board of India’s recent interventions in the valuation framework deserve more attention than they have yet received. Taken together — the revised definition of fair value, the coordinating valuer mechanism, the notification of the International Valuation Standards, the Valuation Report Identification Number regime, and the move toward standardised reporting formats — these are not minor procedural adjustments. They are part of a broader attempt to make insolvency valuation more coherent, more verifiable, and more reliable as an institutional foundation of the IBC process. [1] [2] [3]

The significance of these reforms lies precisely in that institutional ambition. Valuation affects bargaining power, recoveries, plan selection, and litigation risk. It also affects whether market participants believe the process is producing numbers they can rely on. This article argues that the IBBI’s recent valuation reforms are among the most structurally important interventions in the current insolvency reform cycle. They improve the architecture of the valuation ecosystem in important ways. But they do not, by themselves, solve the harder problem: whether insolvency valuation in practice will become accurate, disciplined, and dependable enough to support the commercial legitimacy the system demands.

II. Valuation in CIRP and Liquidation: Different Roles, Same Stakes

Before turning to the recent reforms, it is useful to separate the role valuation plays in the two main insolvency pathways. The function is not identical in CIRP and liquidation, but the stakes are high in both.

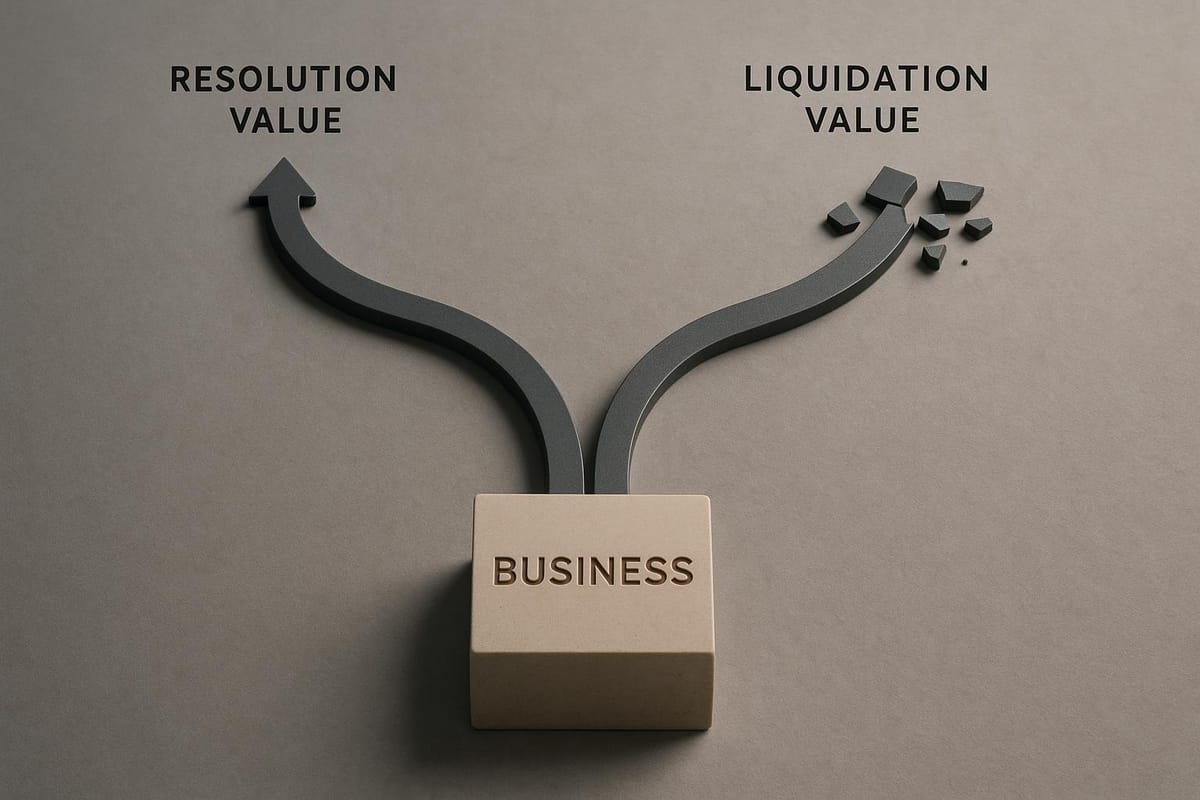

In the Corporate Insolvency Resolution Process, valuation performs two connected tasks. Fair value helps anchor commercial judgment about what the corporate debtor or its assets could command in a properly marketed transaction, while liquidation value provides the downside benchmark against which resolution outcomes must be assessed. In practical terms, these figures influence how the Committee of Creditors evaluates competing plans, how bidders position themselves, and how confidently the process can claim that resolution is preferable to liquidation. [1]

In liquidation, the function changes. The focus shifts from comparing rescue outcomes against a downside floor to managing realisation itself: reserve pricing, sale sequencing, expectation-setting, and distribution discipline. Here too, valuation is not passive background data. If it is too high, it can delay realisation and distort strategy. If it is too low, it can legitimise under-recovery and convert distress into needless value destruction. [1]

The common thread is straightforward. In both CIRP and liquidation, valuation does not merely describe value; it helps shape outcomes around it. That is why errors in valuation travel so far downstream, and why reforming the valuation architecture matters as much as it does.

| Dimension | CIRP | Liquidation |

|---|---|---|

| Core valuation function | Benchmark plan quality, inform CoC judgment, and anchor comparison against the liquidation alternative. | Support realisation strategy, reserve discipline, sequencing, and distribution outcomes in a distress-sale setting. |

| Value logic | Fair value and liquidation value both matter, with enterprise value increasingly important where the business can survive as a going concern. | Focus shifts toward what assets can realistically fetch through managed sale, while avoiding destructive undervaluation. |

| Main decision influenced | Whether a resolution plan is commercially credible and preferable to liquidation. | How assets should be sold, at what reserve expectations, and in what order. |

| Main risk of weak valuation | False optimism, weak CoC bargaining, distorted bidder pricing, and bad resolution selection. | Low reserve pricing, distressed under-recovery, and unfairly compressed realisations. |

III. The Fair Value Redefinition: A Conceptual Shift with Unfinished Edges

One of the most important changes in the recent valuation reforms is the revised definition of “fair value” in the CIRP Regulations. Under the current framework, fair value is the estimated realisable value of the corporate debtor or its assets, as the case may be, if they were to be exchanged on the insolvency commencement date between a willing buyer and a willing seller in an arm’s length transaction, after proper marketing, where the parties had acted knowledgeably, prudently, and without compulsion. The accompanying Explanation further requires that the estimate account for the enterprise value of the corporate debtor, where applicable. [1]

This is not a cosmetic definitional adjustment. It marks a serious attempt to move Indian insolvency valuation away from fragmented asset logic and closer to commercially realistic assessment. Earlier CIRP valuation practice could produce exactly the kind of distortion that weakens decision-making: asset classes were valued independently, the aggregate often lacked conceptual coherence, and the final figure did not always reflect what an informed buyer would actually pay for the business as a functioning or recoverable enterprise. The revised definition pushes the framework toward a more economically honest question — what would this corporate debtor, or its assets, realistically command in a properly marketed arm’s length process at the insolvency commencement date. [1]

The enterprise value dimension is especially important. A distressed company may still be worth materially more as an operating business than as a collection of separated assets. Customers, contracts, workforce continuity, supply-chain position, licences, and market presence can all create going-concern value that a purely asset-fragment approach may miss or discount too heavily. By requiring fair value to take enterprise value into account where applicable, the revised framework better aligns valuation with the way serious buyers assess distressed businesses in the real market.

At the same time, the reform does not eliminate difficulty; it relocates it. The key qualification — “where applicable” — leaves significant room for judgment, and that judgment will often be contested. In some cases, enterprise value may be genuine and material. In others, distress may already have eroded operating viability to such an extent that enterprise value sits only marginally above liquidation assumptions. The challenge is not simply conceptual. It is evidentiary and methodological. Valuers will need to decide when enterprise logic is justified, how heavily it should influence fair value, and how to prevent optimism from being mistaken for commercial realism.

That unresolved judgment call is the real fault line in the revised definition. The reform is important because it recognises that fair value in insolvency should not be trapped inside a narrow asset-by-asset frame. But whether it succeeds will depend on how disciplined valuation practice becomes in applying enterprise value without turning it into an unsupported uplift. The revision improves the conceptual architecture. It does not remove the need for sophisticated professional judgment.

IV. The Coordinating Valuer: Necessary Discipline, Unresolved Influence

Among the recent valuation reforms, the coordinating valuer mechanism is one of the most operationally significant. Under the revised Regulation 35(1)(a), where the corporate debtor has more than one asset class requiring valuation, the appointed set must include one registered valuer for each asset class, and one of them is to be designated as the coordinating valuer by the resolution professional in consultation with the Committee of Creditors. [1]

The commercial logic behind this reform is easy to understand. Multi-asset insolvency valuation can become incoherent when different valuers work in parallel without any structured coordination. Asset classes may be assessed on incompatible assumptions, sector context may be unevenly understood, and the resulting figures may sit beside one another without adding up to a convincing picture of the corporate debtor as a whole. In that setting, the problem is not simply variation. It is fragmentation. A process that relies on valuation to anchor creditor judgment cannot afford a methodology that produces disconnected answers to what is ultimately one commercial question.

The coordinating valuer mechanism is meant to respond to exactly that weakness. The designated valuer must facilitate a meeting in which all registered valuers involved — and, where relevant, other coordinating valuers — explain the methodology being adopted to the resolution professional and the CoC before the reports are finalised. [1] This creates a structured point of methodological discipline that earlier practice often lacked. It should reduce the risk of incompatible assumptions across asset classes and make it easier for the CoC to understand how the valuation exercise is actually being constructed. That is a serious improvement, especially in larger or more complex CIRPs where cross-asset inconsistency can materially distort decision-making.

It also makes the valuation process less opaque. Earlier reform discussions had already recognised the need for valuers to explain methodology before their reports hardened into process facts. [4] The coordinating valuer structure turns that concern into a procedural feature. If used properly, it can strengthen accountability, improve challenge quality, and give creditors better visibility into whether the valuation is commercially coherent rather than merely formally complete.

But the reform also creates a new pressure point. A coordinating valuer is not simply an organiser. In practice, the role may acquire soft authority over how methodology is framed, how disagreements are managed, and which assumptions become dominant in the discussion. That may be entirely benign in some cases. In others, it may create an unacknowledged hierarchy within what is still supposed to be a multi-valuer process.

That matters because the independence of the valuation exercise is not tested only by formal appointment mechanics. It is also tested by professional dynamics. If the coordinating valuer becomes the de facto lead voice, the process may drift from coordination toward influence without ever saying so openly. The risk is not necessarily misconduct. It is subtler: convergence that looks methodologically clean but reflects soft pressure, deference, or process design rather than genuinely independent assessment.

Accountability is another unfinished issue. If a valuation outcome later proves unsound, the current framework does not fully resolve how responsibility should be understood where the coordinating function shaped the methodology discussion but each valuer remained independently responsible for the assigned asset class. That ambiguity may matter in real disputes. Coordination is useful, but once coordination begins to affect substance, the line between facilitation and influence becomes harder to police.

The reform is therefore best understood as both necessary and incomplete. India’s insolvency valuation framework needed a mechanism to reduce fragmentation in multi-asset cases. The coordinating valuer provides one. But it also introduces new independence and perception risks that will need to be watched carefully. In insolvency, coherence is valuable. It just cannot come at the cost of hidden hierarchy.

V. Standards, Verification, and the Risk of False Comfort

The IBBI has recently moved on two related fronts: valuation standards and valuation report discipline. Together, these measures aim to make insolvency valuation more consistent, more comparable, and easier to verify across cases.

The first major step was the Board’s circular dated 1 April 2026 notifying the International Valuation Standards as the applicable standards for valuations conducted under the Code and regulations made thereunder. [2] This applies across CIRP, liquidation, voluntary liquidation, pre-packaged insolvency, and personal guarantor bankruptcy processes. The importance of this move lies not only in the adoption of an internationally recognised framework, but in the fact that it finally replaces an earlier ambiguity. For some time, the regulatory architecture referred to “internationally accepted valuation standards” without actually specifying which standards those were. That left avoidable room for methodological inconsistency. Different valuers could claim broad compliance while still working from materially different assumptions, approaches, or reporting structures. The IVS notification removes that ambiguity.

That is a substantial gain. IVS provides a common professional grammar for valuation work across business assets, real estate, plant and machinery, financial instruments, and intangible assets. It gives insolvency stakeholders a more stable reference point for understanding what a valuation engagement is supposed to look like, how methodology should be framed, and what reporting discipline should accompany the final conclusion. For a system that increasingly depends on valuation reliability, that kind of common baseline matters.

The second front is report integrity and comparability. The February 2026 amendment requiring valuation reports and documentation to be prepared in the Board-notified format adds a layer of standardisation that earlier practice lacked. [1] The VRIN regime, introduced through the August 2024 circular, pushes in the same direction by requiring every valuation report to carry a Valuation Report Identification Number generated through the IBBI portal. [3] Together, standardised formatting and report identification make it easier for creditors, resolution professionals, tribunals, and regulators to compare reports, verify provenance, and reduce the risk of unverifiable or irregular valuation documents circulating in the process.

These are real improvements. Standardisation matters because valuation reports do not operate in a vacuum. They are read by creditors with uneven technical expertise, relied on by professionals under time pressure, and tested in proceedings where procedural confidence often matters almost as much as substantive reasoning. A common reporting structure and verifiable report identity make the ecosystem easier to navigate and harder to game.

But this is also the point at which reform can generate false comfort. A valuation report may be neatly structured, IVS-aligned on its face, and properly authenticated through VRIN, yet still rest on weak data, strained assumptions, or poor commercial judgment. Formal discipline improves trust only up to a point. After that, it can create the illusion that process cleanliness equals substantive correctness.

Standardisation can improve comparability. It cannot itself guarantee sound valuation.

Verification can establish report authenticity. It cannot establish that the number is commercially persuasive.

A system that mistakes formatting discipline for valuation reliability risks becoming more orderly without becoming more accurate.

The IBBI’s moves on IVS, report format, and VRIN should therefore be welcomed for what they are: an important strengthening of the valuation infrastructure. But they should not be mistaken for a complete solution. In insolvency, disciplined presentation is valuable. It is not a substitute for disciplined judgment.

| Recent valuation reform | Intended benefit | Critical concern |

|---|---|---|

| Revised fair value definition | Moves valuation closer to realistic arm’s-length exchange logic and permits enterprise-value thinking where appropriate. | “Where applicable” leaves room for interpretive inconsistency and valuation spread. |

| Enterprise value explanation | Better reflects going-concern upside instead of pure asset-fragment logic. | Can be overstated if distress, weak data, or thin buyer markets are not judged carefully. |

| Coordinating valuer | Improves cross-asset consistency and makes methodology discussion more structured for the CoC. | May create hidden hierarchy, dependence effects, or blurred accountability if not managed carefully. |

| IVS + prescribed format + VRIN | Raises comparability, authenticity, and documentation discipline across insolvency valuations. | Can create false confidence in neatly formatted outputs even when underlying assumptions remain weak. |

| MSME proportionality debate | Potentially lowers cost and friction for smaller debtors. | May weaken the challenge function precisely where information quality is often already fragile. |

VI. The MSME Proportionality Debate: Efficiency Versus Fragility

The question of how valuation rules should apply to MSME corporate debtors is one of the most revealing unresolved policy debates in the current framework. On one view, the standard valuation architecture used in CIRP can be too heavy for smaller enterprises. On another, simplifying valuation in the MSME context may weaken safeguards precisely where the information environment is already most fragile.

The case for proportionality is not difficult to make. The conventional two-valuer-per-asset-class structure, together with the broader expectations of coordination, documentation, and methodology discipline, was built with larger and more complex debtors in mind. For smaller enterprises, the same framework may impose costs that are disproportionate to the value being preserved, delay cases that should move faster, and place procedural demands on insolvency participants that the economics of the case may not justify. If the aim of insolvency law is to preserve value efficiently, there is a genuine policy argument for asking whether the same level of valuation architecture is necessary in every MSME case. [1]

That instinct, however, runs straight into a harder truth. MSMEs often do not present cleaner valuation environments than larger companies. In many cases, they present messier ones. Financial records may be incomplete, governance practices may be informal, related-party arrangements may be harder to disentangle, asset ownership may be imperfectly documented, and audited data may be less robust. In other words, the smaller size of the enterprise does not necessarily reduce valuation risk. It may increase it.

That is what makes the MSME debate harder than it first appears. The most intuitive case for simplification is cost. The strongest argument against simplification is reliability. A lighter valuation framework may reduce expense and friction, but it may also remove exactly the duplication and challenge function that help protect against weak assumptions, thin data, or professional overconfidence. A single-valuer or otherwise simplified arrangement may look proportionate on paper while making fragile cases even more dependent on one judgment call.

The policy dilemma is therefore not simply whether MSMEs deserve a streamlined process. It is whether the system can simplify valuation without sacrificing the minimum safeguards needed for trustworthy outcomes. That would require more than reducing procedural steps. It would require thinking carefully about substitute safeguards: what level of documentation must remain compulsory, what disclosure discipline is needed, what challenge mechanisms can replace duplication, and how independence and competence are to be preserved in a simplified model.

This is where the proportionality debate becomes genuinely important. The cases that appear easiest to streamline may be the very cases in which valuation fragility is greatest. If reform focuses only on procedural efficiency, it may produce a framework that is cheaper but less reliable. If it ignores proportionality altogether, it risks forcing smaller debtors through a valuation architecture whose cost and complexity are commercially misaligned. The right answer is not obvious. But any serious solution will need to acknowledge that MSME simplification is not a low-risk administrative tweak. It is a question about how much valuation uncertainty the insolvency system is willing to tolerate.

VII. What the New Ecosystem Could Achieve

If these reforms are implemented well, they could materially improve insolvency valuation in India in four connected ways.

They could improve consistency by reducing the risk that multiple asset-class valuations are assembled into a commercially incoherent whole. The coordinating valuer mechanism and the methodology discussion before reports are finalised both push in that direction. The IVS framework also gives valuers and stakeholders a shared professional language. [1] [2]

They could also improve comparability. Standardised report formatting and the VRIN system make valuation reports easier to read, authenticate, and compare across cases. That matters not only for resolution professionals and creditors, but also for tribunals and regulators trying to assess whether a valuation exercise was properly carried out. [1] [3]

They could improve the link between valuation and commercial decision-making. A process in which methodology is explained before reports are finalised should produce better-informed creditor oversight and stronger challenge quality. Creditors do not need to become valuers. But they do need enough visibility into valuation logic to understand what they are relying on when making high-stakes decisions. [1] [4]

They could also professionalise the market over time. A clearer standards framework, better reporting discipline, and stronger verification architecture should raise baseline expectations across the valuation ecosystem. That would not eliminate poor practice. But it should make weak practice easier to identify and harder to defend.

None of these gains is automatic. But taken together, they show why the current reform package matters. It is trying to make insolvency valuation not only more formalised, but more dependable as a foundation for commercial judgment.

VIII. What Could Still Go Wrong Despite Reform

The recent reforms improve the valuation framework, but they do not remove the core risks that make insolvency valuation difficult in practice.

The first is data quality. Valuation can only be as reliable as the information on which it rests. Where the corporate debtor’s records are incomplete, liabilities are imperfectly disclosed, related-party dealings are opaque, or business performance data is unstable, even a technically compliant valuation may still be materially unreliable. The problem is not that the framework lacks standards. It is that standards cannot fully repair bad inputs.

The second is the persistent difficulty of valuing businesses in distress. The revised fair value definition is designed to reflect a properly marketed arm’s length exchange, and that is conceptually sound. But distressed markets rarely behave cleanly. Buyers are fewer, caution is higher, discounts are sharper, and comparable transactions are often poor guides. In that environment, the line between commercial realism and excessive pessimism is difficult to draw. Enterprise value may be real, but so is the risk of overstating it when market confidence has already eroded.

The third risk is institutional overconfidence in formatted outputs. A report that is IVS-aligned, properly structured, and VRIN-authenticated may still be weak in substance. That matters because insolvency systems often reward documents that look orderly. But valuation reliability does not come from formatting alone. If creditors, professionals, or tribunals begin to treat formal compliance as a proxy for commercial soundness, the system may become more orderly without becoming more trustworthy.

The fourth is capacity. A more demanding valuation regime requires a deeper pool of professionals who can handle distress-specific judgment, sector complexity, and methodological scrutiny under real time pressure. If the registered valuer ecosystem lacks that depth, the reform programme may raise formal expectations faster than the market can credibly meet them.

The fifth is independence. The more central valuation becomes to plan comparison, reserve logic, and process legitimacy, the more damaging any perceived compromise in independence becomes. Even where conflicts are not provable, the appearance of influence can reduce confidence in the output and intensify challenge risk.

Each of these risks has a downstream cost. Weak data produces questionable numbers. Questionable numbers produce discounted bids, contested assumptions, and weaker creditor confidence. That in turn increases litigation, reduces process legitimacy, and can directly affect recoveries. The real test of the current reform cycle is not whether valuation reports become more standardised. It is whether insolvency outcomes begin to rest on numbers that market participants actually trust.

IX. Valuation as a Legitimacy Mechanism

The deepest case for correct valuation in insolvency is institutional, not technical.

When valuation is trusted, it stabilises the process. Creditors can treat it as a serious benchmark rather than a ritual document. Resolution applicants can price against it with greater confidence. Tribunals can scrutinise disputes against something more credible than competing assertions. In that sense, valuation does more than inform decision-making. It helps make high-stakes decision-making defensible.

The reverse is equally true. When valuation is distrusted, the damage spreads quickly. Bidders discount more aggressively. Creditors become less confident in plan comparisons. Challenges intensify. Litigation becomes easier to sustain because the numerical foundation of the process itself is in doubt. A valuation regime that lacks credibility does not merely weaken one stage of insolvency. It weakens the legitimacy of the entire process.

That is why the IBBI’s recent interventions matter. The revised fair value definition, the IVS notification, the coordinating valuer mechanism, the VRIN regime, and the move toward standardised reporting should all be understood as efforts to strengthen the legitimacy infrastructure of insolvency valuation. They are trying to make the numbers more coherent, more comparable, more transparent, and more defensible.

That is the right project. But legitimacy is earned in use, not declared in rules. The reforms will matter only if they produce valuations that are not just formally compliant, but genuinely credible to the professionals, creditors, tribunals, and buyers who must rely on them.

X. Conclusion

Correct valuation matters in insolvency and liquidation because too much depends on it for it to be treated as a technical side-function. It shapes bargaining, informs creditor judgment, influences plan pricing, affects reserve discipline, and underpins the credibility of both resolution and liquidation outcomes.

Seen in that light, the IBBI’s recent reforms are more than compliance adjustments. The revised fair value definition, the coordinating valuer mechanism, the IVS notification, the VRIN system, and the move toward standardised reporting all represent an effort to make insolvency valuation more coherent, more transparent, and more reliable as a decision-making foundation under the Code. Taken together, they amount to one of the more important structural reform clusters in the current insolvency cycle. [1] [2] [3]

But the real test lies beyond architecture. Better definitions, better coordination, recognised standards, and cleaner report formats do not automatically produce trustworthy valuation outcomes. That depends on data quality, sectoral competence, methodological discipline, independence, and the willingness to confront distressed reality without either false precision or disguised optimism.

The IBBI has improved the framework. Whether the reform succeeds will depend on whether practice now produces valuations that creditors, tribunals, and the market can genuinely rely on. That is where this programme will finally be judged.

References

[1] Insolvency and Bankruptcy Board of India (Insolvency Resolution Process for Corporate Persons) Regulations, 2016 — consolidated text as amended up to 25 February 2026. Available at: https://ibbi.gov.in/uploads/legalframwork/25bb769595e91be71dec98cfc447ea78.pdf

[2] IBBI Circular — Valuation Standards for the purpose of valuation conducted under the Insolvency and Bankruptcy Code, 2016, dated 1 April 2026. Available at: https://ibbi.gov.in/uploads/legalframwork/b176b05d02cba50ae0d3279ff6ed553e.pdf

[3] IBBI Circular — Generation of Valuation Report Identification Number (VRIN) for valuation conducted by Registered Valuers under the Insolvency and Bankruptcy Code, 2016, dated 12 August 2024. Available at: https://ibbi.gov.in/uploads/legalframwork/fec61f0798e424d32aa521af3e82f344.pdf

[4] IBBI Discussion Paper on Amendments to CIRP Regulations, 2016, dated 1 November 2023. Available at: https://ibbi.gov.in/uploads/whatsnew/b70daeb0fbec8cc61d1afc52e9e9fbb8.pdf

Disclaimer: This article is published for academic and educational purposes only. It does not constitute legal advice or a legal opinion. It was prepared with AI assistance and reviewed before publication. Readers should consult the relevant laws, regulations, and cited source materials before relying on any proposition discussed here.

Subscribe for new article alerts

Receive an email when a new Insolvation article is published. No unrelated marketing.

Collected here: your email address and consent proof for article-alert delivery. Purpose: confirmation and new-article alerts. Retention: active while subscribed, with suppression records retained after unsubscribe to honor your opt-out. Details: Privacy notice · Privacy rights.